|

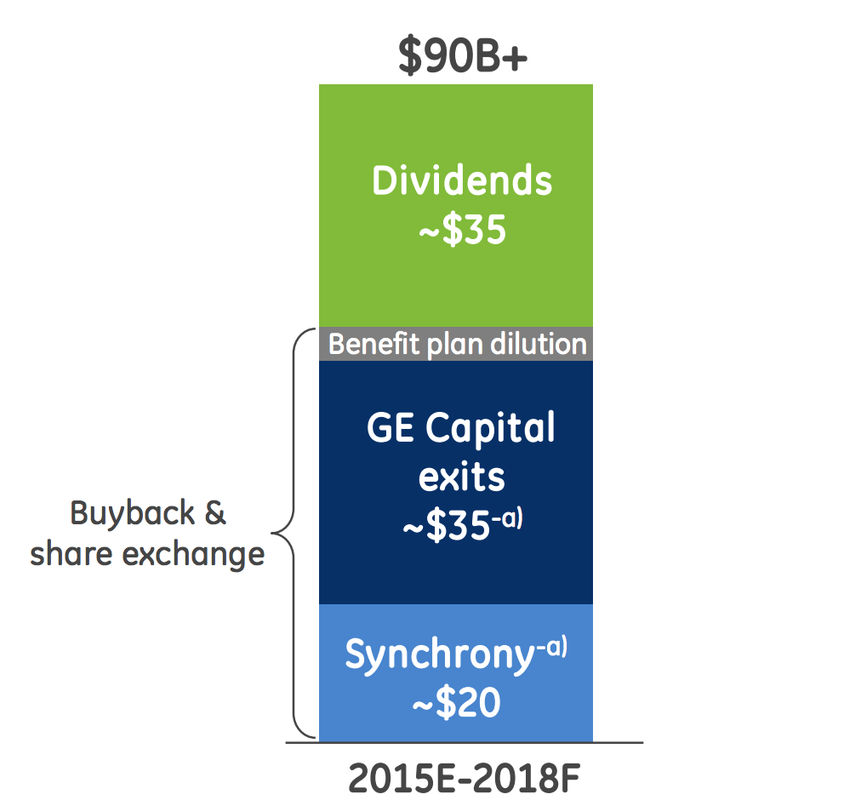

Company Overview General Electric is an America industrial company with exposures to many different sectors. The company has operations in: power and water, oil and gas, energy management, aviation, healthcare, transportation, and appliances. The company made an attempt to diversify into financial services through GE Capital, but has since been divesting their financial business lines. The company has recently sold its private equity lending business to the Canadian pension plan, for a cash consideration of $12 billion. This divesture is line with management’s goal to become a pure play industrial company. Additionally the financial assets on the balance sheet had the potential to make General Electric a systematically important financial institution; this would expose the company to more stringent regulations. Ridding itself of these business lines will allow management to return more capital to shareholders through repurchases and dividends. The company has announced a new repurchase program; the company has the ability to purchase $50 billion in shares through 2018. This repurchase plan indicates management’s willingness to return capital to shareholders. Potential For Acquisitions General Electric is shedding over $200 billion of assets in its financial operations divestment. The company will look to add more industrial assets with the new capital, and increased borrowing capacity. The company will look to build out its life sciences division. Life science device companies as opposed to other industrial areas are higher growth and less capital intensive. The company will look to make acquisitions in the multi billion-dollar range that will fit with the company’s shareholder return plans. The company may also choose to buy oil and gas service assets as current market dynamics offer compelling return profiles. At current price level the company may take a run at an oil services firm like National Oilwell Varco, though this remains unlikely. The company would also like to complete their deal of Alstom’s power business. Regulatory approval for the deal is expected to come by August 21st. General Electric’s CEO Jeff Immelt in the latest conference call, reaffirmed his believe that the Alstrom deal still offered significant value for shareholders. Cash Flow Generation & Underlying Operations General Electric has $90 billion in cash on its balance sheet, an indicator that the operations of the business have been able to generate significant cash. The company has a growing order backlog of $261 billion; this represents almost two years of annual revenue. The company is able to operate at a 16.2% margin, indicative of the pricing power of their business lines. The industrial segment of the business was able to increase margins by 50 basis points in 2014. The company forecasts earnings growth of 14.5% to 20% from their industrial segment in the 2015 fiscal year. Currently the industrial segment represents 65% of company earnings, but is expected to grow to 90% by 2018. General Electric is set to capitalize on the world making large investments in infrastructure projects over the next 20 years. It is expected that the world will spend cumulatively $70 trillion on infrastructure spending by 2035. The company should have stakes or roles in many of these projects moving forward. Increased government spending to replace ageing infrastructure will fuel the growth for General Electric’s industrial operations. The company has highly engineered products in the power generation field, these products will benefit from continued increased environmental regulation. With increasing investments into railroads, because of fuel and cost efficiencies; the company should see increased sales of its locomotives. General Electric has ramped up its focus on providing services to clients. The company has offerings in software, intelligent machines, and big data. The division has done $46 billion in sales in 2014, and expects much more in 2015. The service backlog has increased from $180 billion to $189 billion. The service division operations operate at a 32% margin, this shows the value the company brings to clients. The company was able to work with Norfolk Southern a train operator, to increase their network velocity by 10%. The services division was able to reduce the fuel usage at Air Asia generating a cost savings of $10 million. The service division also was able to help a utility increase their wind turbine output by 4%. These projects deliver considerable cost savings to their clients, and are an integral part of General Electric’s business moving forward. Investment Thesis Ridding itself of the financial services lines of business, will give the company significantly less exposure to risky decision-making. The industrial business lines General Electric is operating in are benefiting from a quickly changing world. As the world becomes more complex, the demand for highly engineered solutions has increased. These highly engineered solutions in areas like software and big data have greatly benefited General Electric’s services division. As companies demand more ways to integrate technology into their businesses, General Electric will offer innovative solutions. With earnings from industrial operations growing at rates of 16% annually the dividend can be increased easily over time. Even if the company aims for significant dividend growth there will be excess earnings that can be reinvested into back into the company. These reinvested earnings will generate capital gains for shareholders. Currently General Electric creates $14 billion in free cash flow, representing a 5% return on market value. This return growing in these high growth business lines will adequately compensate shareholders. The company expects to keep the dividend flat until 2016, choosing instead to focus on share buybacks. With the significant cash hoard the company has, it has the ability to put that cash to work repurchasing shares. Below is the potential returns to shareholders over the next three years.

0 Comments

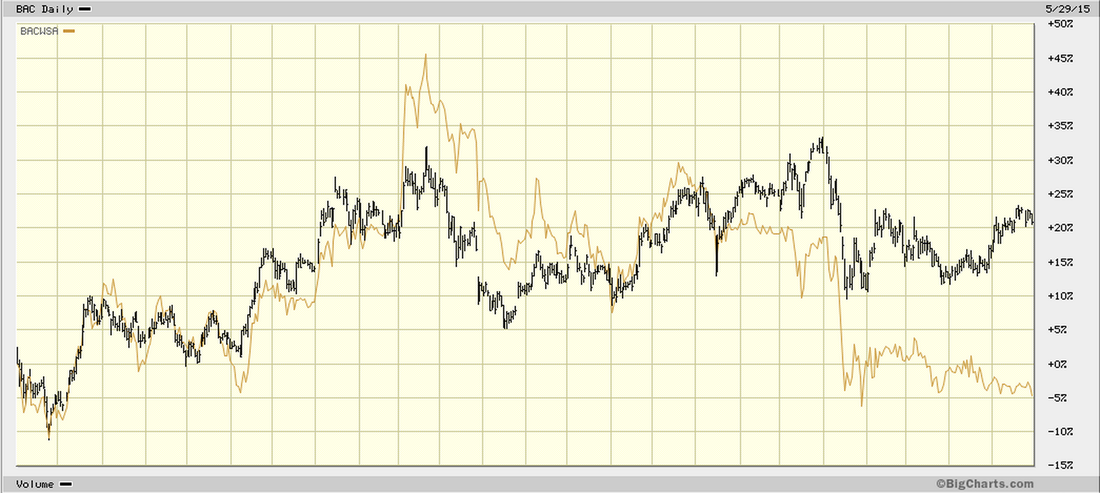

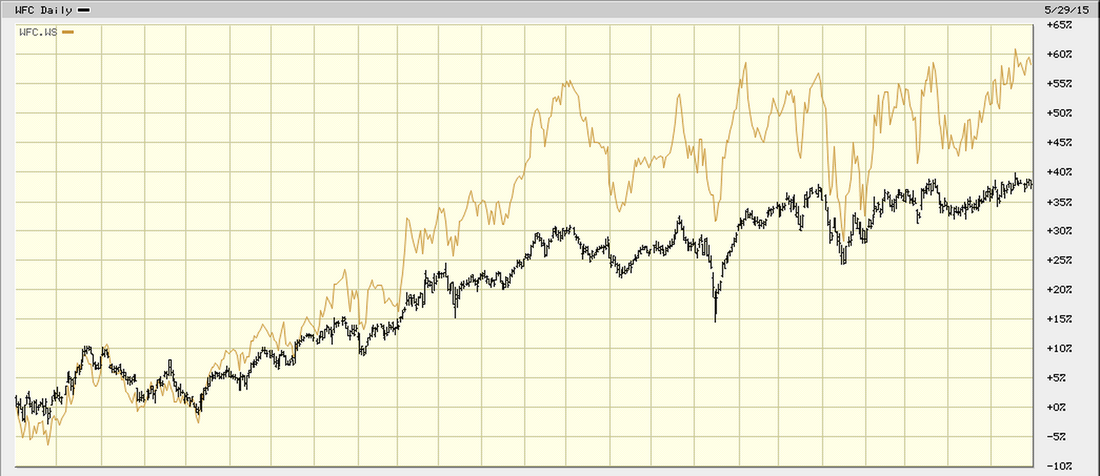

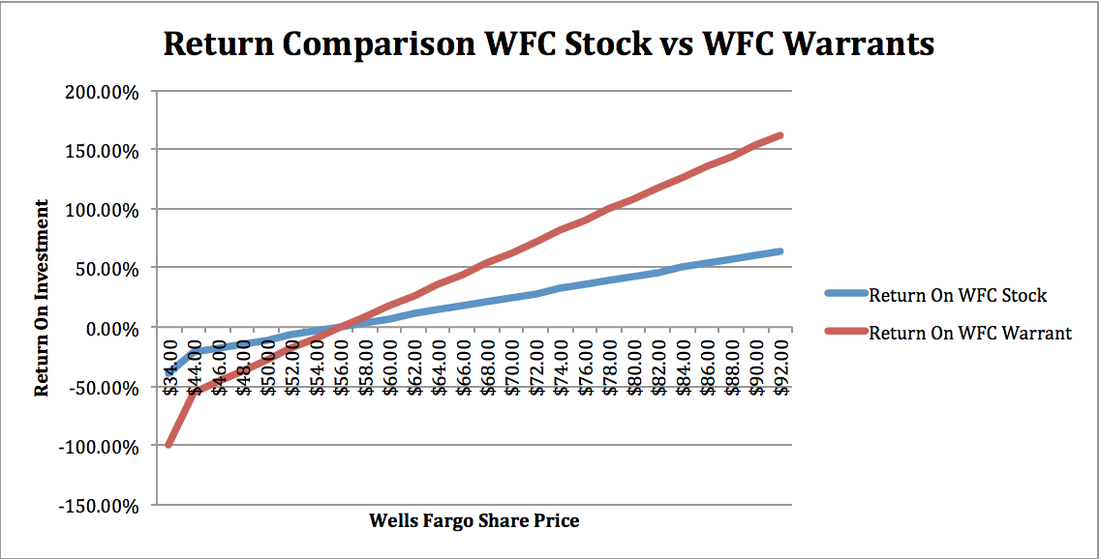

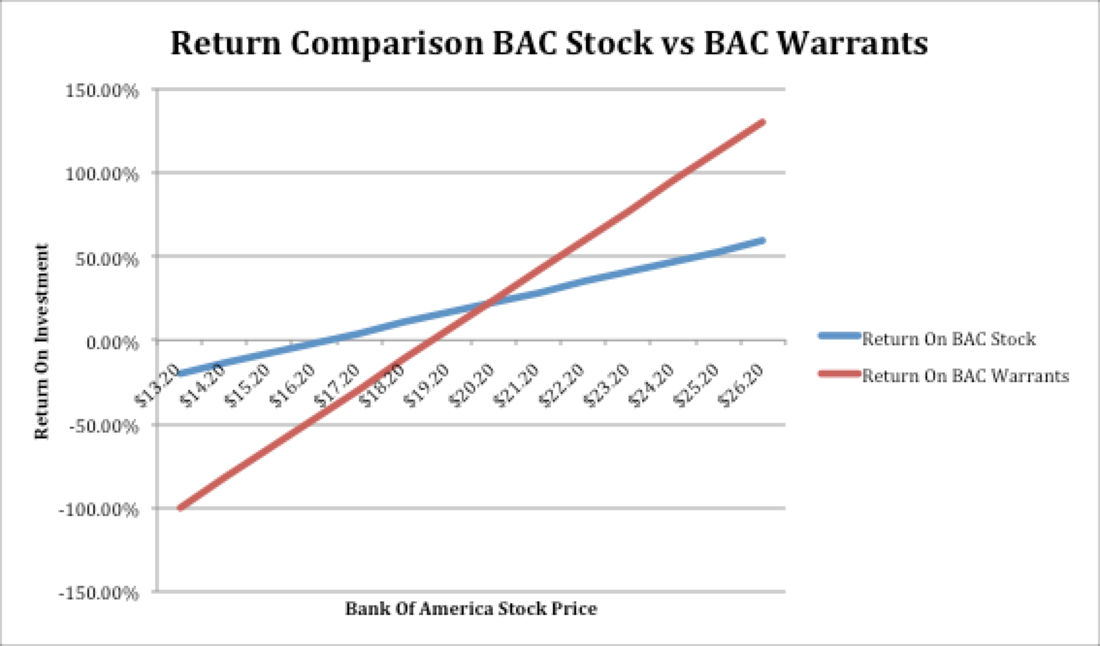

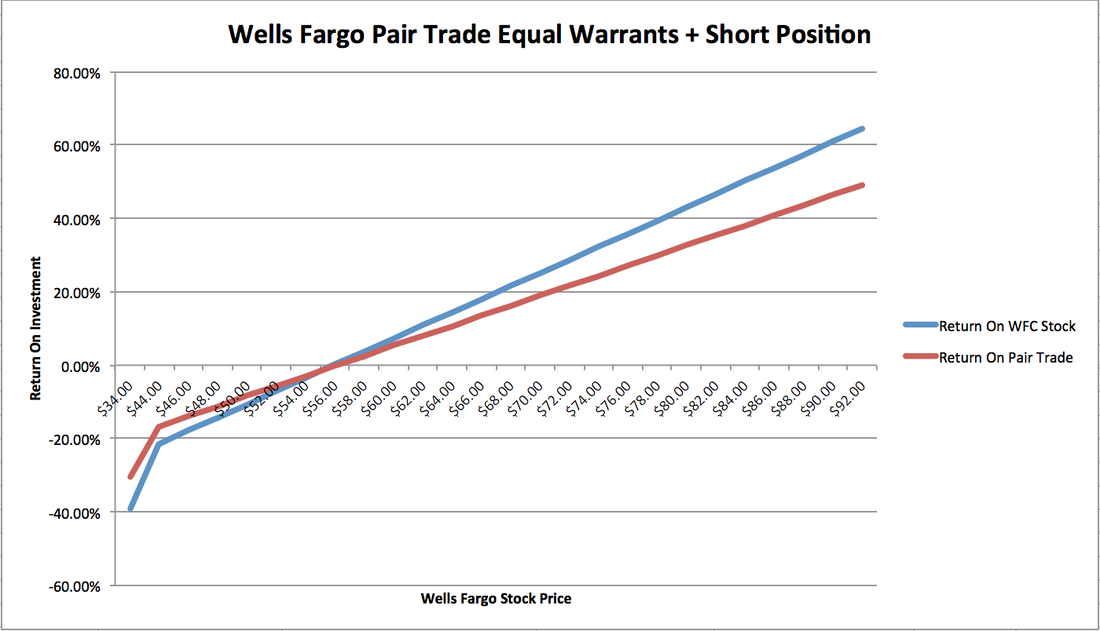

Warrants Overview Both Wells Fargo and Bank of America issued long dated warrants back in the depths of the great recession. The Wells Fargo warrant expires October 2018, while the Bank of America warrant expires in January 2019. The two graphs below depict the two-year performance of each of the warrant contracts compared to their underlying common shares. As can be seen the Wells Fargo warrants have outperformed the common by a widening margin, as the common shares have increased. The opposite can be said for the Bank of America warrants, as the common shares have increased; the warrants have underperformed by a widening margin. The asymmetric trends between these two warrants are interesting to explore. To better understand these trends I conducted an analysis of the underlying value of each warrant based on prices of May 31, 2015.   Return Comparison Between Warrants The assumption I made was that the Bank of America warrants would offer better upside than the Wells Fargo warrants. The Bank of America warrants should in theory offer more upside as they have considerably more downside risk. A 20% decrease in the Bank of America current stock price, would render the warrants worthless. For Wells Fargo a 40% decrease in stock price would render the warrants worthless, this adds additional safety on a comparative basis. The interesting trend I discovered was that if both underlying stock increase the same amount on a percentage basis, the Wells Fargo warrants have a higher return. The reason for this I concluded to be, investors see a considerable more upside in the underlying value of Bank of America shares than in Wells Fargo shares. This seems to make sense as Bank of America is trading under tangible book value, while Wells Fargo trades at 1.77 times it’s tangible book value. The tables and charts below try to depict a picture of the returns of each warrant.   Investment Rationale It can be seen from the tables above that at the current prices, the Wells Fargo warrants look like a rewarding play. For Wells Fargo bulls the math is simple, a 21.54% return in the underlying common share results in a 53.92% return in your warrant investment. This would mean the stock has to average a 7% return over the next three years, this does not seem like an extraordinary event. The warrant investor’s return would be an annualized 18% return. However, any investor in these warrants needs to have considerable risk tolerance, as any correction in the market will result in magnified losses. The Bank of America warrants also have a rewarding return profile, and potentially greater upside. The greater upside arises from the fact that the underlying stock of Bank of America appears more undervalued. There is less downside protection on the Bank of America warrants, so investors have to tread carefully. Both these warrant investments seem like rewarding plays for an enterprising investor with these three characteristics: long term bull on banks, wants to achieve large returns, and one who has a tolerance for risk. Pair Trade Potential The reason for purchasing these warrants is the considerable outsized returns on the upside. As can be seen from the charts above, the divergence of the stock and warrant return becomes exponentially larger with increases in the underlying stocks. To protect yourself on the downside, without giving up too much upside, you can hedge the warrant trade. If you short the underlying stock and make a warrant investment, you can achieve a net long position. This would also protect some of, but not all of the downside potential. Another potential pair trades could be buying the warrants and selling long dated calls on either of the stocks. Or an investor could buy the warrants and buy long dated puts. The appeal of the warrant investment is enormous upside, but investors who want to temper their enthusiasm can utilize a pair trade to hedge the downside risk. If any reader would like me to explore a pair trade from a mathematic perspective, I can make an attempt to model the returns.  |

AuthorRotman MBA Student interested in common stock investing, with a preference for high cash-flow businesses. Archives

December 2020

Categories |

RSS Feed

RSS Feed