|

CSG Systems International, Inc. Company Overview CSG Systems International, Inc. CSGS provides business support solutions primarily to the communications industry globally. The company offers revenue management and digital monetization solutions, including Advanced Convergent Platform, a cloud-based platform; and Ascendon, Singleview, Total Service Mediation, and Wholesale Business Management Solution platforms. These platforms enable these media firms to facilitate customer transactions through traditional and emerging channels such as streaming services and cable. These solutions provide critical infrastructure for media firms to engage with their customers. Thesis As media firms and other content providers expand into new channels and offer customers content through digital formats, CSG will play a critical role in developing revenue management and analytics capabilities within these channels. COVID-19 has accelerated the push for media companies to release and provide content to customers online. In the latest quarterly conference call, the firm’s management highlighted the robustness of their sales pipeline and the appetite for cloud-based solutions. There are many opportunities for the firm to incrementally increase revenue by generating new customer relationships globally, entering new verticals, and through strategic acquisitions. An example is a recent deal with JP Morgan to support credit card customer relationship management, with the goal of preventing fraud-related activity. The firm operates in the vertical software market that is characterized by key attractive features. Customer relationships are supported by large-scale multi-year contractual agreements, they recently extended their service agreement with Comcast for 5 years. The cost for a customer to replace CGS as a solution provider is large. Significant software customization is required to configure the solutions to industry-specific and customer specifications. CGS’s niche focus on Media and Telecom gives the firm a competitive edge when competing against larger software providers. Investors will continue to become interested in the shares of CGS due to the firms’ conservative valuation and fast-growing dividend. I believe the shares are worth between $60-$80 per share based on very conservative estimates of Free Cash Flow. Dividend Growth Story CGS Systems is a very strong dividend growth story, with a dividend CAGR of 10.9% over the last seven years. This dividend growth has been supported by growth in net income, as the payout ratio of the firm has continued to hover between 35-45%. The current dividend yield of 2.2%, represents an appetizing yield for long-term oriented investors. This is supported by a strong cash generative business underpinned by long-term contracts with premier customers. Revenue Mix and Quality CGS has significant client relationships that account for a considerable amount of their revenue in Comcast (23%) and Charter Communications (21%). This exposes them to the risk of the loss of a major client. However, CGS has been taking steps to diversify its revenue base to other industry verticals. Since 2015, CGS has reduced revenue from Traditional Media from 68% of revenue to 58%. Over 80% of CGS’s revenue comes from the Americas, thus opportunities exist for the firm to generate more business globally. Increasing revenue diversification has been a priority for the management of CGS. Although, many growth avenues remain with existing Telcom and Media clients. For example, Xfinity a unit of Comcast recently came to CGS to help them deploy the Ascendon cloud platform to improve the customer acquisition process. This deployment specifically targeted the customer lifecycle management of college-aged streaming service clients. Analyst Coverage and Investor Recognition CGS is an under-covered stock that has not received enough attention from both equity research analysts and retail investors, only three major analysts currently cover the stock. The majority of CGS’s shares are held by institutions that do not actively trade the shares. Renaissance Technologies a leading hedge fund has a >5% stake in the firm, indicating a bullish perspective on the stock. Acquisitions CGS made two sizeable acquisitions in 2018, Business Ink, Co ($70 million) and Forte Payment Systems ($85 million), Inc. This acquisition activity will support the business in staying ahead of curve in payment servicing and outsourcing solutions. These deals also enable CGS to begin exploring additional verticals to service including financial services and healthcare. Investors will reward CGS management if they can build a more diverse revenue base, resulting in less exposure to the Media and Telecom sectors. Catalysts

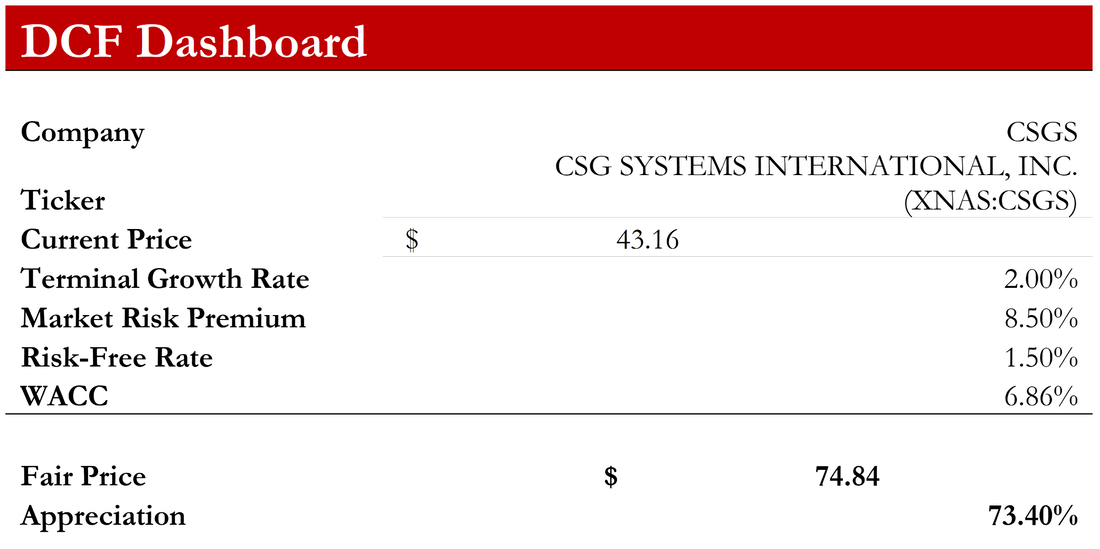

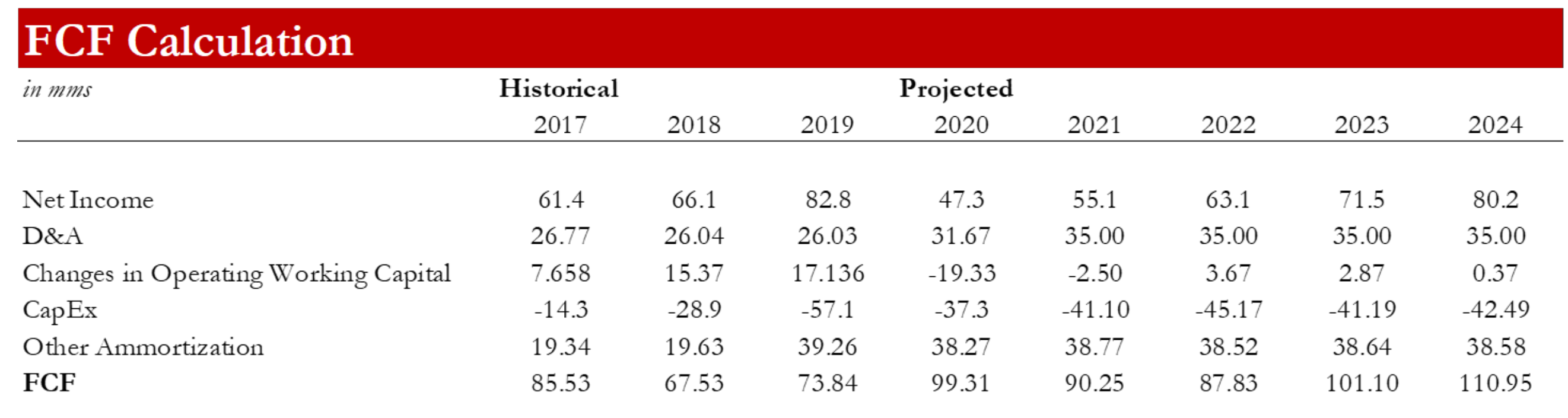

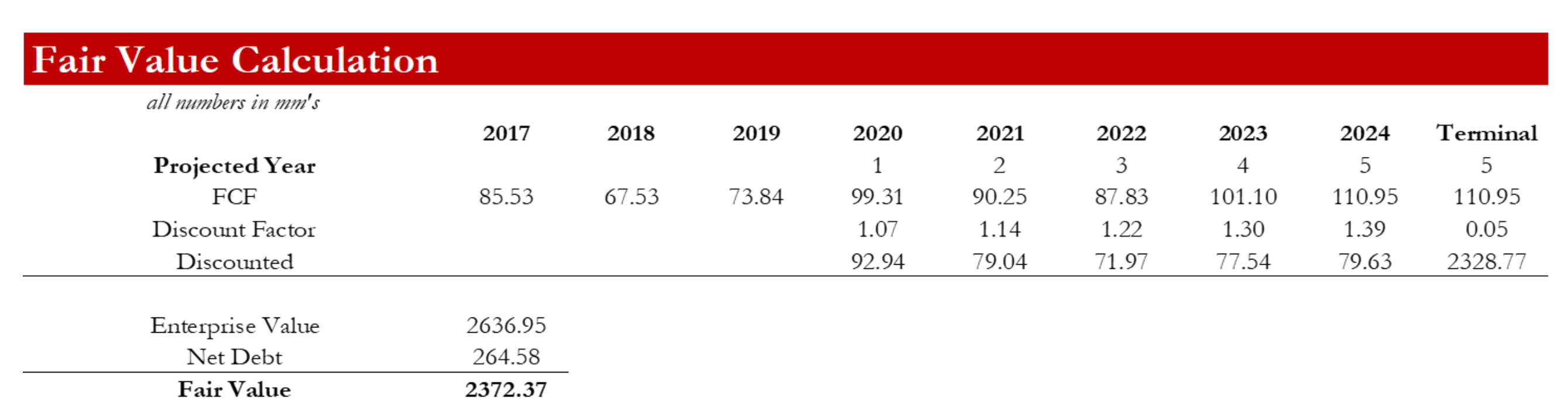

Valuation Based on a discounted cash flow analysis of CGS Systems International, I came to a fair value of the shares of $74.84 Per Share. This valuation is supported by robust cash flow and a supportive market backdrop of record-low interest rates. This price represents a 73.40% upside from the most recent closing price of $43.16. I believe the major catalyst for stock price appreciation is dividend growth milestones. CGS will become a dividend growth leader, this will encourage many new investor bases to explore this stock. Appendix – DCF Valuation

0 Comments

|

AuthorRotman MBA Student interested in common stock investing, with a preference for high cash-flow businesses. Archives

December 2020

Categories |

RSS Feed

RSS Feed